It’s Called Recovery, but Where’s the Beef?

Many economists and other analysts have recognized that the recovery from the U.S. economy’s most recent contraction has been unusually weak—weaker, for example, than any other since World War II. But analysts have disagreed in characterizing the current recovery, which according to the National Bureau of Economic Research, the semi-official arbiter of business-cycle chronology, began in mid-2009 after a contraction that had continued for ten quarters. Some aspects of the economy, such as real GDP and consumer spending, have recovered their pre-recession highs and continued to increase. The rate of unemployment has fallen by several percentage points from its high of more than 10 percent. Net private business investment, which took an especially steep tumble during the contraction, has regained much of its loss.

Some of the most-cited indexes of recovery, however, are ambiguous, at best. The rate of unemployment, for example, has fallen in large part because millions of potential workers have left the labor force. The employment/population ratio, which fell by about 5 percentage points during the contraction, has barely budged from its new, much lower plateau. A growing GDP, despite its near-universal acceptance as the best measure of economic growth, actually tells us little about changes in the public’s well-being. Some components of GDP, especially some of the elements that pertain to government spending, actually should be deducted from, rather than added to, the domestic product, inasmuch as the related government activities—military aggression abroad, domestic spying on the entire population, enforcement of counter-productive and even destructive regulations, prosecution and incarceration of people whose “crimes” have no victims—harm the public, rather than improving their welfare.

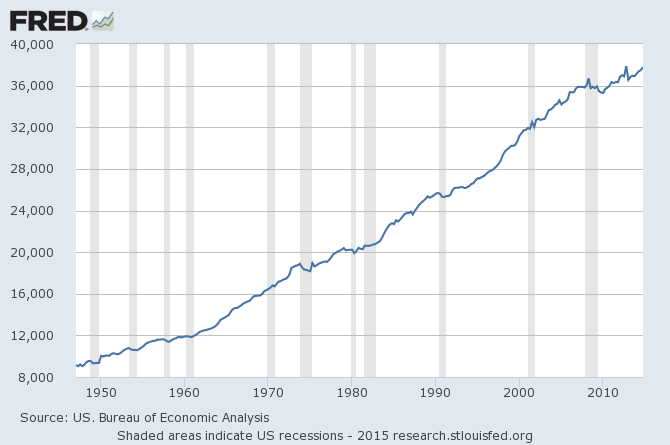

Arguably the best single, currently available measure of the entire public’s payoff from economic activity is real disposable income per capita. This is the average amount per annum that Americans receive in exchange for the use of their labor and other input services, after taxes, corrected for changes in the purchasing power of the dollar. As the chart below shows, this measure of economic well-being has scarcely increased at all since 2007.

Real Disposable Personal Income per Capita (chained 2009 dollars)

To give greater precision to one’s visual impressions, I have computed the average compound rate of growth of the variable in the succeeding stages of faster or slower growth visible in the chart. The results are as follows:

| Period | Average annual percentage rate of growth |

| 1949–1961 | 2.2% |

| 1961–1973 | 3.7% |

| 1973–1983 | 1.3% |

| 1983–1996 | 2.1% |

| 1996–2007 | 2.4% |

| 2007–2014 | 0.6% |

These figures demonstrate that even though the rate of increase has varied substantially in the past, it has never remained so low as it has been in recent years. Even during the decade of so-called stagflation from the early 1970s to the early 1980s, real disposable income per capita grew more than twice as fast as it has grown in the past seven years. In the past, recessions were always followed by relatively brisk growth during the first several years of the ensuing recovery. Such has not been the case this time. Nor do forecasters anticipate any such surge of growth in the future. Might it be that the state’s burdens loaded onto the private producers of wealth—taxes, regulations, uncertainties, intrusions of all sorts, including demands for elaborate reports, asset seizures, and threats of felony prosecution for completely innocent and harmless actions—have finally become the “last straw” for these long-suffering camels?

However that may be, the current situation is clear enough. The U.S. economy, though not yet completely stagnant, has made little headway for more than seven years, and there is little reason to foresee any great change in this regard. Although some indexes of economic performance have recovered substantially since mid-2009, others have done so much less or not at all. And, without a doubt, the alleged recovery process has failed to deliver the “beef” that means the most to the people: substantial growth of real disposable personal income per capita.

{kind=link}