How Much Longer Can the U.S. Economy Bear the Burdens?

Ordinary people, and sometimes experts as well, tend to overreact to short-term economic changes. The current economic malaise in the United States and Europe has brought forth a bevy of commentators convinced that this time the economy has taken a permanent turn for the worse. Never again, they declare, will we enjoy growing prosperity as we did in days of yore. Some of these Chicken Littles do see a possible means of escape from the impending doom, but only if the government carries out an extraordinarily bold economic rescue program, flush with such Keynesian measures as unprecedented monetary “quantitative easing” and large ongoing deficits in the government budget. Anything else, they insist, condemns us to languish indefinitely in a “liquidity trap” characterized by diminished rates of employment and slow, if any, economic growth. Economic historians know, however, that such declarations are hardly new and that the economy’s long-run trend has continued to tilt upward for two centuries despite the short-run ups and downs around the trend line.

Nevertheless, even the experts perceive some ominous longer-term changes and appreciate that people, in the conduct of their economic affairs, may have limits to how many burdens they can bear. These burdens take the form of taxes, regulations, and uncertainties loaded onto them by governments at every level. Each year, for example, federal departments and regulatory agencies put into effect several thousand new regulations. Only rarely do these agencies remove any existing rules from the Code of Federal Regulations. Thus, the total number in effect continues to climb relentlessly. The tangle of federal red tape becomes ever more difficult for investors, entrepreneurs, and business managers to cut through. Business people have to bear not only a constantly changing, ever more complex array of taxes, fees, and fines, but also a larger and larger amount of regulatory compliance costs, now estimated at more than $1.8 trillion annually. Governments at the state and local levels contribute their full share of such burdens as well. Small wonder that the economic freedom rank of the United States among the world’s nations has fallen substantially in recent years.

So it is scarcely a wild-eyed question if we ask, as economist Pierre Lemieux does in a probing article in the current issue of Regulation magazine, whether the U.S. economy is now reacting to these growing burdens by undergoing “a slow-motion collapse.” A substantial body of evidence supports the answer that indeed such is the case.

To examine some of the most important such evidence, I have divided the U.S. economy’s post-World War II history into three periods: 1948-1973, 1973-2007, and 2007 to the present (or the most recent date for which appropriate data are available). These periods are defined by apt demarcations in that each of the years 1948, 1973, and 2007 was a business-cycle peak. Measuring longer-term changes between business cycle peak years is a time-honored way in which economists guard against drawing faulty conclusions by comparing conditions in essentially noncomparable years, between, say, a cyclical peak year and a cyclical trough year or between a peak or a trough and an intermediate year somewhere in the intervening contraction or expansion.

Consider first the average annual rate of growth of real (that is, inflation adjusted) GDP per capita. From 1948 to 1973, this rate was 2.5 percent. Between 1973 and 2007, however, it was only 1.8 percent. And between the fourth quarter of 2007 and the fourth quarter of 2014, it was a mere 0.4 percent per annum. Thus, the average rate of real economic growth has slowed substantially during the past 67 years, and the current anemic recovery from the cyclical trough reached in mid-2009—the weakest recovery of any since World War II—may be only a continuation and worsening of a deteriorating growth performance that stretches back more than 40 years.

Let us examine next, therefore, the long-run growth performance of the major economic input, which is hours of labor applied in production processes. It is easy to muddy the water in this regard if we include all workers, because a a substantial number of workers are, and long have been, employed by governments, which need not make the same kinds of economic calculations and appraisals that private employers must make. No dispassionate observer can deny that much government employment is, and always has been, make-work—employment created for political motives by public-sector employers who need not worry about a bottom-line constraint and can rely on the capture of funds via taxes, fines, fees, and forfeitures to meet their payrolls. Indeed, many government employees—for example, tax collectors, drug warriors, vice cops, domestic spies, and most regulatory enforcers—are engaged not so much in make-work as in anti-work, efforts that serve only to harass and harm the public at large, and, truth be told, they subtract from rather than adding to the true social product. In assessing the economy’s long-term health, therefore, we must confine our attention to private workers, who help to produce goods and services that are genuinely valued by consumers in free markets.

Consider then the number of persons engaged as wage and salary earners in private nonfarm employment. Between 1948 and 1973, the average annual rate of growth of such workers was 1.9 percent. Between 1973 and 2007, it was only slightly less at 1.8 percent. Between December 2007 and December 2014, however, this rate of growth collapsed to a mere 0.3 percent per annum. Whatever else we may say about the current recovery, it has scarcely touched the heart of the problem in the labor markets. Indeed, millions of potential workers have dropped out of the labor force entirely, surviving on savings, disability insurance benefits, unemployment insurance benefits, other welfare benefits, and the generosity of kinfolk. Whatever the most accurate description of recent events in the labor markets may be, there is no gainsaying the reality that potential workers who are no longer working are doing nothing to assist in the overall economy’s genuine recovery.

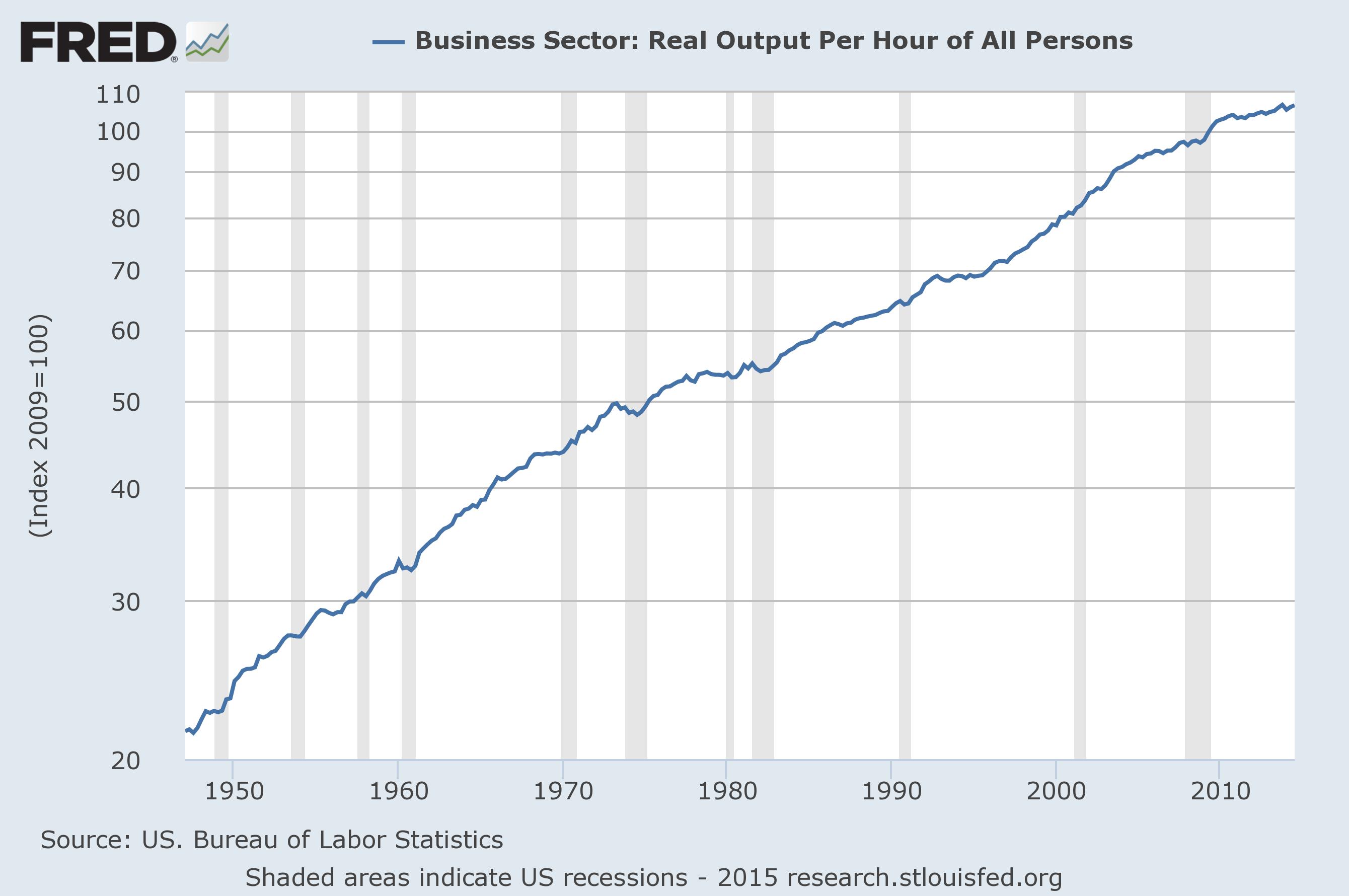

Growing prosperity depends not only on a growing volume of employment but, more important, on the growth of labor productivity brought about by capital accumulation, technological and organizational changes, and improvements in the health, education, and training of the labor force. Again, to see what has happened on this critical front, we must concentrate on the private sector. Here we find that between 1948 and 1973, the average annual rate of growth of real output per hour worked in the business sector was 2.7 percent. From 1973 to 2007, however, this growth rate was only 1.9 percent per annum, and between the fourth quarter of 2007 and the third quarter of 2014 it was even less, just 1.3 percent per annum. Clearly many employers who have been reluctant to hire new workers since the economy’s cyclical trough in mid-2009 have been able to squeeze more output from the same number of workers during the past five years, but notwithstanding these efforts the rate of growth of labor productivity has been substantially slower than it was during the preceding 60 years. Perhaps we are indeed witnessing more than a weak cyclical recovery. In Figure 1, which I have plotted on a logarithmic scale, the declining rate of growth of private output per hour can be seen clearly as a reduction in the slope of the line after 1973 and, even more so, after 2005 or thereabouts.

Figure 1. Real Output per Hour in the U.S. Business Sector, 1947-2014

There is much more to this story than I have space to mention here. It must suffice to say that the present anemic recovery fits into a much longer-term pattern of declining economic robustness in the U.S. economy’s performance. (A similar story can be told about western Europe.) Although various hypotheses may plausibly be advanced to account for this pattern, it makes good economic sense to interpret the economic history of the past several decades as the tale of a camel on which, without a doubt, more and more straws have been piled. Although the beast’s back is not yet broken, his powers have surely been tested severely, and as additional burdens continue to be loaded onto him year after year it is an open question as to how much longer he will be able to make any headway at all. Adam Smith wisely observed that “[t]here is a great deal of ruin in a nation,” but he did not say that there is an infinite amount. It is a mistake to suppose that no matter how greatly the governments of the United States burden the nation’s private sector, they can never crush the life out of it.

{kind=link}