Wendy’s Won’t Use Dynamic Pricing—But Should They?

They’re dead to me,” was the reaction of one friend when he learned of the plan, now characterized as an alleged plan, to introduce Uber-style surge pricing to Wendy’s fast food restaurants. No sooner did I begin writing this article (including the following line: “Given the initial reaction, it’s possible that the Wendy’s surge pricing plan will never see realization.”) than the company issued a statement saying that it would not implement those pricing methods. It characterized a phrase that CEO Kirk Tanner used during the 4th quarter conference call indicating that Wendy’s “w[ould] begin testing more enhanced features like dynamic pricing and daypart offerings along with AI-enabled menu changes and suggestive selling” as “misconstrued.”

I have no problem giving Wendy’s the benefit of the doubt, although the management might have said that truly dynamic pricing would see prices rise and fall. That might have deflected some of the hysteria, which included calls for a boycott and accusations of (intended?) price manipulation, but perhaps not.

It’s no coincidence that the suggestion of responsive pricing is coming in close proximity to the President using Super Bowl LVIII as a platform for bashing private firms over shrinking product sizes and the Fed pushing back against rate cut expectations. The general price level is continuing to rise, and to do so at a pace faster than it has for many years. What the various indices are expressing in a single number, whether it’s the Consumer Price Index (CPI), the Personal Consumption Expenditure Price Index (PCE), or any other, obscures the fine structure of inflationary effects. Obvious, though it seems, an occasional reminder that Americans don’t eat, live in, or fuel their vehicles with the CPI is in order. It’s the prices of specific foods, actual rent, gasoline at the pump, and of innumerable types and amounts of resources that impact every transaction undertaken on a given day. The firms they patronize are also dealing with price increases that impact their ability to offer goods and services to consumers. And all the while, government officials are trying desperately to deflect blame for policies they either put in place or supported.

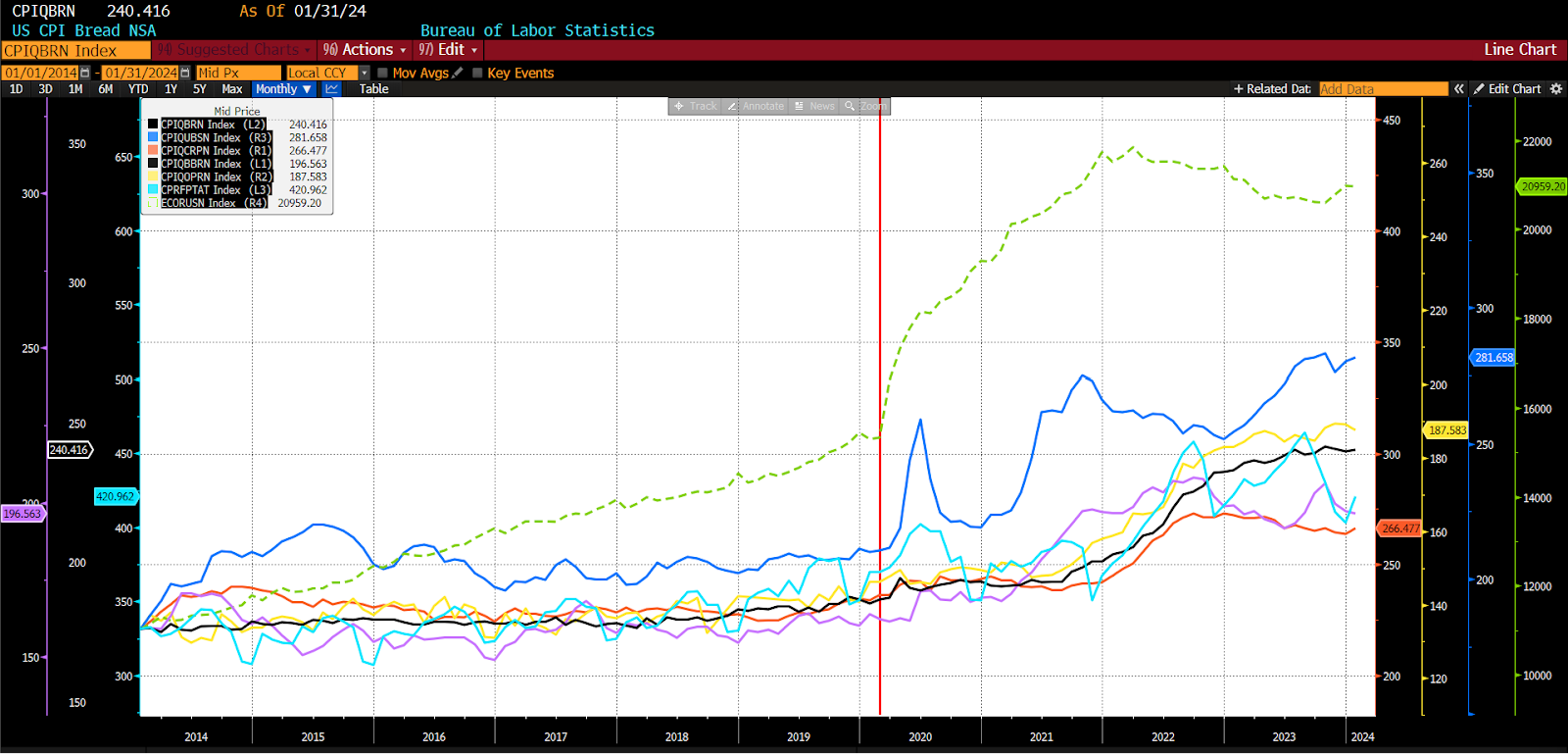

In the below chart are ten years of CPI subindices covering monthly price changes for fast food-proximate products, including bread, uncooked beef, cheese, breakfast sausage and bacon, pickles and relish, and potatoes (in lieu of french fries). The red line indicates the start of the Federal Reserve’s monetary policy responses to the COVID-19 pandemic in March of 2020, with the dashed green line showing the M2 money supply, not seasonally adjusted.

(Source: Bloomberg Finance, LP)

Below are the changes in those food indices from January 2014 to March 2020 and from March 2020 to January 2024. Additionally, the standard deviation and range for each of those indices over the pre-and post-COVID monetary policy period are shown as a proxy for the increasing unpredictability of those prices. Menu costs are those expenses incurred by firms when they have to change prices more frequently as a result of inflation, and it’s not surprising that with a sizable jump in both the cost and volatility of inputs, responsive pricing strategies would be considered by producers. An additional wrinkle: minimum wages are set to rise substantially in many US states in 2024.

| US CPI Uncooked | US CPI Cheese | US CPI Bacon | US CPI Pickles, | |||

| US CPI Bread | Beef | & Related Products | & Breakfast Sausage | Relish, & Olives | US CPI Potatoes | |

| 01/31/2014 | 176.0 | 181.5 | 221.0 | 159.1 | 133.4 | 331.4 |

| 03/31/2020 | 187.3 | 211.6 | 236.6 | 161.5 | 147.7 | 373.1 |

| Percent increase | 6.40% | 16.60% | 7.06% | 1.55% | 10.67% | 12.59% |

| Standard deviation | 2.0 | 5.5 | 3.2 | 4.4 | 4.7 | 18.7 |

| Range | 12.8 | 38.7 | 19.1 | 21.9 | 17.2 | 71.7 |

| 03/31/2020 | 187.3 | 211.6 | 236.6 | 161.5 | 147.7 | 373.1 |

| 01/31/2024 | 240.4 | 281.7 | 266.5 | 196.6 | 187.6 | 421.0 |

| Percent increase | 28.35% | 33.15% | 12.21% | 21.67% | 27.02% | 12.83% |

| Standard deviation | 15.2 | 20.1 | 9.5 | 10.1 | 10.5 | 30.1 |

| Range | 54.3 | 71.7 | 36.3 | 46.6 | 43.5 | 113.4 |

Surge pricing existed long before Uber began using it to price ridesharing services in high volume periods. Electricity, airline tickets, lodging, and other products have been priced according to exigent supply and demand conditions for decades. Congestion pricing on highways is a variant of surge pricing as well. The discount shelf in your lower supermarket is emblematic of the same process as well, albeit in the opposite direction. Variable pricing permits improved resource allocations, including of labor, by responding to real-time conditions. Rising prices at peak demand or usage times improves the reliability of service by discouraging users not in urgent need (or desire) of a good or service to wait until prices are preferable to them. Part of corporate financial sustainability derives from attempting to optimize inventory management. The effect on any firm’s bottom line from preparing products in anticipation of a rush that doesn’t materialize or being unprepared for a deluge of buyers should be obvious. Within the framework of food service, where freshness and perishability loom, make the criticality of inventory management all the more clear.

Backpedaling aside, it would be better for both Wendy’s and Wendy’s customers if (for example) the cost of a sausage, egg, and cheese biscuit and coffee were to rise 50 cents or a dollar at 7:30am when the drive-thru line reaches or exceeds 15 waiting vehicles. Dedicated customers who are likely to be less price sensitive will bear the price increase in high-demand periods, while other, less devoted consumers may look elsewhere. Similarly benefitting would be those customers who enjoy offbeat products at unpopular times of the day: hash browns at 5pm would likely be deeply discounted, perhaps even drawing in customers not typically frequenting Wendy’s.

Whether the employment of dynamic pricing is, in fact, off the table or resurfaces at a later date, it’s instructive to view proposals embracing fluctuating prices alongside mounting accounts of shrinkflation. Both are responses to unanticipated changes in the cost of doing business and are related to pressures on profit margins. In the former case, prices are adjusted to reflect changes in demand that weigh more heavily on resources and generate opportunity costs. In the latter, the firms opt to change the packaging size or ingredients of a good or service to purposely avoid raising consumer prices. Both involve attempts to secure profitability and maintain competitiveness.

In neither case are the two least desirable outcomes chosen: an across-the-board price increase or the outright removal of the good or service from the market. While politicians offer their stock-in-trade— lies, evasion, and pandering—at increasing real costs to American citizens, actual producers are struggling to find ways to continue to serve consumers without losing their shirt—and being threatened for it.

In the last two years, Americans have been urged to believe that inflation is worse everywhere else in the world (it’s not, even now), as well as that gas station owners, Vladimir Putin, corporate profit margins, ocean shipping firms, and greed are to blame for prices rising faster than they have in four decades. All but the most somnolent or ideologically incarcerated minds will receive those assertions with substantial skepticism: that at precisely the same moment in 2021, tens of thousands of businesses of various types and sizes suddenly became more avaricious than they’d been in two generations—and, that their rapacity has also been subsiding in lockstep since mid-2022. While economics is a social science, one needn’t possess a formal education to distinguish broadly rising costs as a systemic matter. And in that light, to view proposals for changing pricing conventions and product packaging as another symptom, rather than a source, of Americans’ large and growing financial hardship.

This article was adapted from AIER.org. You can read the original here.