Fiscal Federalism Turned Upside-Down

A recent study from the American Enterprise Institute (AEI) found that many states misused federal aid related to the pandemic. Instead of using funds for projects related to healthcare, education, and infrastructure, state politicians used the lion’s share of federal funding for the general fund and public pensions.

Aside from the blatant misuse of federal dollars, this study highlights another important issue: state and local government dependence on funding from the federal government. The more states are dependent on DC, the more control DC has over state and local fiscal affairs. When DC inevitably cuts funding to the states, fiscal crises are bound to occur.

AEI’s study found that state government revenues and spending “increased by around 70 cents per incremental windfall dollar of committed federal funds by 2022.” States where public employees had the most influence over pension fund boards saw the largest increases in pension contributions with those federal dollars.

While this misuse of funds is no surprise to many of the critics of federal pandemic aid, it should be shocking to the average American. Despite the US Treasury explicitly banning the use of federal funds for pensions and tax cuts, it still occurred. Evidence from the research shows “no observed increases in liquid cash positions and essentially full spending of received aid.”

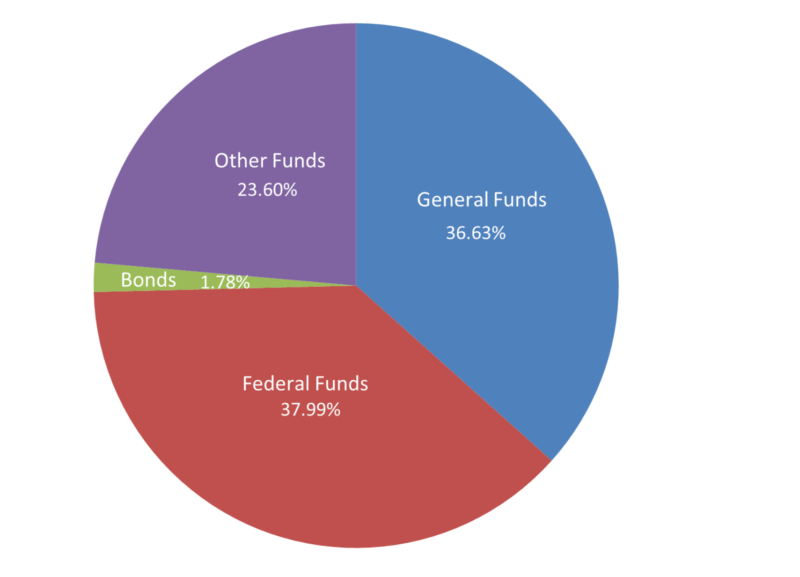

In this case, states must obligate federal money from the American Rescue Plan (ARPA) by December 31, 2024. They then have until December 31, 2026, to spend it or give it back to the federal government. Incentives matter, and in a case of “use it or lose it,” states will find ways for the money to be spent. The latest data show that the average state gets 38 percent ($21.6 billion) of its revenue from federal funds, the largest single category. Expenditures funded by general fund revenue make up the second largest category of expenditures ($20.9 billion). Other funds include revenue sources that are restricted by law for specific functions or activities (gas taxes for a transportation fund, tuition and fees for higher education, or provider taxes for Medicaid) make up the third largest category ($13.5 billion). Bonds make up the smallest category of expenditures ($1 billion), although bond types included in the calculations vary by state.

State Budget Expenditures (Capital Inclusive) by Source, 2022 (50 State Average)

(Source: Authors’ Calculations, National Association of State Budget Officers State Expenditure Report Historical Data)

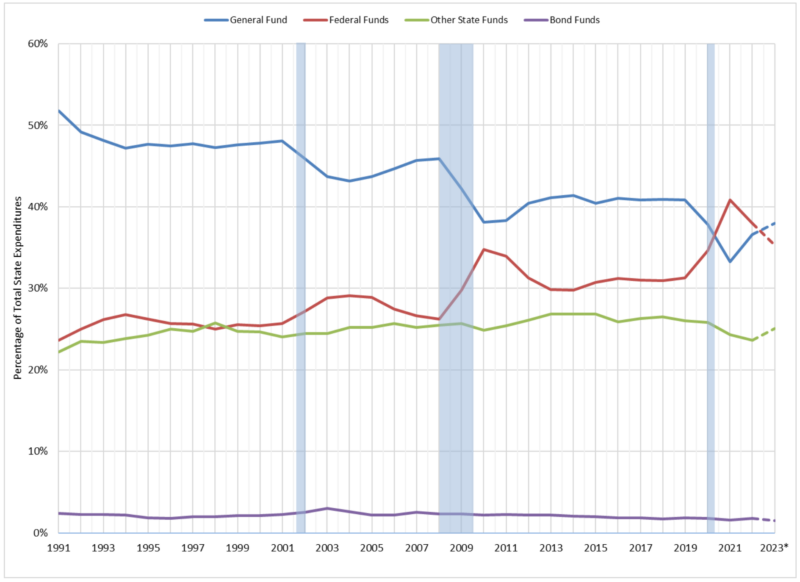

Unfortunately, this is not a new development. Since 1991 (the earliest data available), federal funds have steadily increased as a share of total expenditures at the state level. The chart below shows that the largest increases in federal funds to the states occurred immediately following recessions. Out of fear of losing revenue, state officials seek aid from the federal government, which is more than happy to oblige.

It is a manifestation of the Public Choice concept “the ratchet effect,” where federal spending spikes immediately after a recession or emergency, then lowers when the crisis subsides, but never down to pre-crisis levels.

State Budget Expenditures (Capital Inclusive) by Source as a Percentage of Total Expenditures, 1991-2023

(*2023 totals are projected

Note: Shaded areas indicate periods of recession

Source: Authors’ Calculations, National Association of Ste Budget Officers State Expenditure Report 2023 and Historical Data)

The National Association of State Budget Officers (NASBO) also projects that 2023 data will show that general fund expenditures will exceed federal fund expenditures for the first time since 2020, yet it is not expected to return to 2019 levels. With federal money from ARPA still left to spend, federal funds will likely still make up at least a third of the average state budget.

Like so much else in government spending, the trend is unsustainable. The most recent Financial Report of the United States Government concludes by saying that “[t]he projections in this Financial Report indicate that if policy remains unchanged, the debt-to-GDP ratio will steadily increase throughout the projection period and beyond, which implies current policy under this report’s assumptions is not sustainable and must ultimately change” (emphasis added).

That untenability, furthermore, has not gone unnoticed. In August 2023 Fitch Ratings downgraded the US credit rating from AAA to AA+, the second following the August 2011 lowering by Standard and Poor. In November 2023, Moody’s Investment Service changed the US credit outlook to negative. Lower credit ratings threaten higher interest costs on an already massive amount of government debt. These rising costs and debt will force lawmakers in Washington to make some difficult cuts to spending. When the time comes to make painful cuts, politicians in DC will cut funding to the states, expect state leaders to deal with the funding issues, and let them take the blame for the inevitable tax hikes and spending cuts.

Most US states ended FY 2021, 2022, and 2023 with budget surpluses. Many states took the opportunity to focus on tax relief, switching from graduated income taxes to flat income taxes. While the flat tax revolution helped many Americans keep more of their hard-earned money, the gains will be for naught if states do not properly control spending.

The best way for states to rein in spending is by enacting constitutional rules at the state level such as the Taxpayer’s Bill of Rights (TABOR) in Colorado. TABOR limits the growth of government to the maximum growth of population plus inflation, requires any taxes collected in excess of that limit to be refunded to taxpayers with interest, and requires voter approval before new taxes. This rule also applies to local governments, so the state cannot grow government by way of unfunded mandates on local governments. TABOR, however, does not apply to federal funds given to Colorado.

Another example is provided by Utah, which established the Financial Ready Utah program in the wake of the Great Recession. This package of bills requires state agencies to have emergency plans in place for anywhere between a 5-percent to 25-percent reduction in funding and requires state agencies to seek legislative approval before applying for federal funds.

State-level constitutional limits on taxes and spending provide greater protection from reckless government spending than relying on the “right” candidates to win elections or the “right” bureaucrats to be appointed. When government actors are bound by strong institutional constraints regarding political instincts and incentives toward reckless spending, already-overtaxed citizens needn’t rely on wishful thinking.

This article was originally posted on AIER.org. You can read the original here.